Featured

Table of Contents

For those ready to take a little bit much more danger, variable annuities use extra possibilities to grow your retirement possessions and potentially increase your retirement revenue. Variable annuities supply a series of investment options looked after by expert cash supervisors. Because of this, financiers have a lot more flexibility, and can even relocate properties from one option to another without paying tax obligations on any kind of financial investment gains.

* A prompt annuity will certainly not have an accumulation phase. Variable annuities issued by Safety Life Insurance Company (PLICO) Nashville, TN, in all states except New York and in New York by Safety Life & Annuity Insurance Policy Company (PLAIC), Birmingham, AL.

Capitalists ought to thoroughly think about the investment objectives, risks, costs and expenditures of a variable annuity and the underlying financial investment alternatives prior to spending. An indexed annuity is not an investment in an index, is not a safety or stock market investment and does not take part in any type of supply or equity investments.

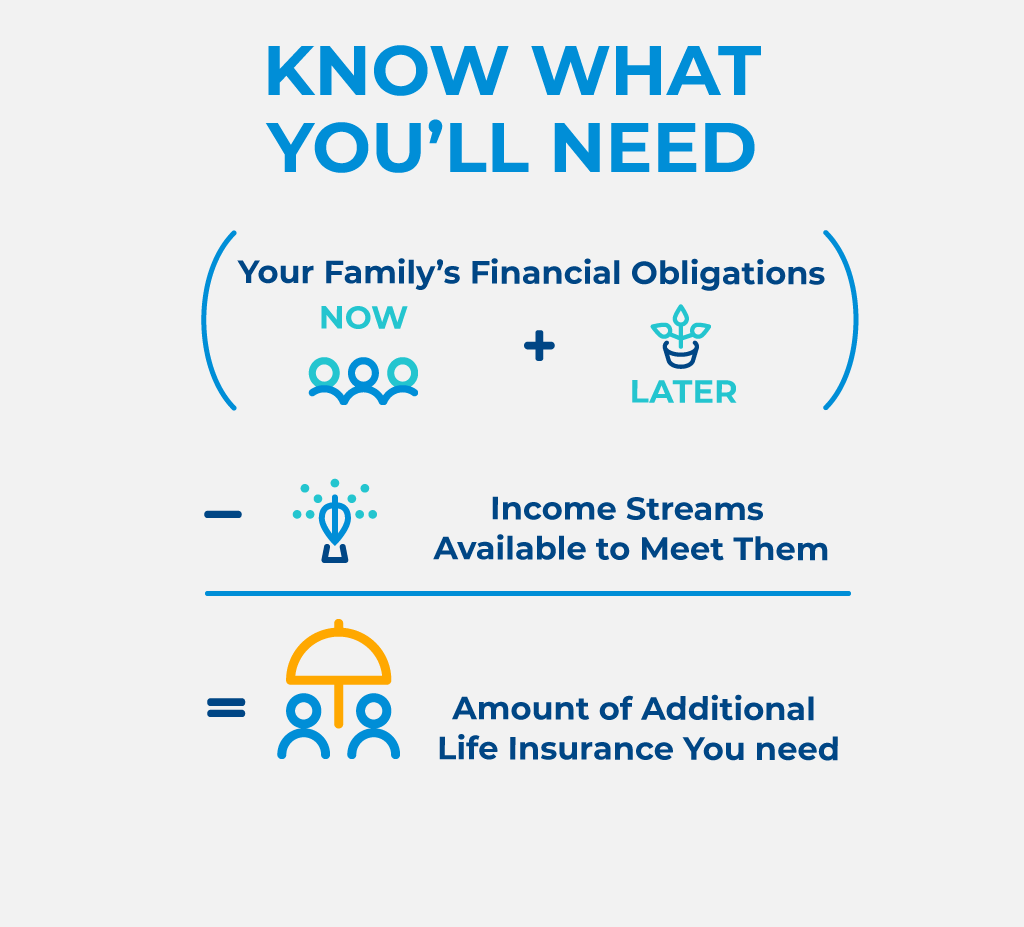

What's the distinction in between life insurance and annuities? It's a typical inquiry. If you question what it requires to protect a monetary future on your own and those you like, it may be one you find yourself asking. Which's a very good point. The lower line: life insurance policy can aid give your loved ones with the financial peace of mind they should have if you were to die.

Who should consider buying an Retirement Income From Annuities?

Both must be thought about as component of a long-term economic plan. Both share some resemblances, the general objective of each is very various. Allow's take a glimpse. When comparing life insurance policy and annuities, the largest distinction is that life insurance coverage is developed to aid secure against a monetary loss for others after your fatality.

If you intend to discover a lot more life insurance policy, checked out up on the specifics of how life insurance works. Think about an annuity as a tool that can help satisfy your retired life requirements. The main objective of annuities is to create revenue for you, and this can be carried out in a couple of various means.

What is the most popular Fixed-term Annuities plan in 2024?

There are several possible advantages of annuities. Some include: The capability to grow account value on a tax-deferred basis The possibility for a future revenue stream that can not be outlasted The possibility of a round figure benefit that can be paid to a making it through partner You can acquire an annuity by giving your insurance policy company either a single round figure or making repayments with time.

:max_bytes(150000):strip_icc()/Secondary-Market-Annuity.asp-Final-1ca20750b00e46cd955fba96155eeb3a.png)

Individuals normally buy annuities to have a retired life income or to develop cost savings for an additional purpose. You can purchase an annuity from a qualified life insurance policy representative, insurer, financial planner, or broker. You ought to speak with a financial consultant concerning your requirements and goals prior to you buy an annuity.

Why is an Annuities For Retirement Planning important for long-term income?

The difference in between the two is when annuity settlements begin. enable you to save money for retired life or other reasons. You don't have to pay taxes on your profits, or contributions if your annuity is an individual retired life account (INDIVIDUAL RETIREMENT ACCOUNT), up until you take out the earnings. allow you to create an earnings stream.

:max_bytes(150000):strip_icc()/Immediate-variable-annuity.asp-final-c62d88ef3f7a4b688c0303ef04e1fbce.png)

Deferred and instant annuities supply a number of alternatives you can pick from. The alternatives supply different degrees of potential risk and return: are assured to gain a minimum rates of interest. They are the most affordable economic threat yet supply reduced returns. make a higher rate of interest, yet there isn't a guaranteed minimum interest price.

allow you to pick in between sub accounts that are similar to mutual funds. You can gain a lot more, but there isn't an ensured return. Variable annuities are greater danger since there's a possibility you might lose some or every one of your cash. Set annuities aren't as dangerous as variable annuities since the financial investment danger is with the insurer, not you.

If performance is low, the insurer bears the loss. Fixed annuities guarantee a minimum interest price, usually between 1% and 3%. The company may pay a greater rates of interest than the guaranteed rate of interest. The insurance provider establishes the interest prices, which can alter regular monthly, quarterly, semiannually, or yearly.

Can I get an Immediate Annuities online?

Index-linked annuities show gains or losses based on returns in indexes. Index-linked annuities are a lot more complex than fixed postponed annuities. It is essential that you recognize the functions of the annuity you're considering and what they suggest. Both contractual attributes that impact the amount of interest attributed to an index-linked annuity one of the most are the indexing approach and the participation rate.

Each relies upon the index term, which is when the company computes the interest and credit scores it to your annuity. The establishes just how much of the boost in the index will certainly be used to calculate the index-linked interest. Other essential attributes of indexed annuities include: Some annuities cap the index-linked rate of interest.

Not all annuities have a flooring. All dealt with annuities have a minimum surefire value.

Variable Annuities

Other annuities pay substance passion during a term. Compound interest is passion gained on the cash you conserved and the rate of interest you gain.

This percent could be made use of as opposed to or in enhancement to an involvement rate. If you take out all your cash before the end of the term, some annuities won't attribute the index-linked rate of interest. Some annuities might attribute only part of the interest. The percent vested usually boosts as the term nears the end and is constantly 100% at the end of the term.

How long does an Annuity Accumulation Phase payout last?

This is due to the fact that you bear the investment danger instead of the insurer. Your representative or economic adviser can aid you make a decision whether a variable annuity is right for you. The Stocks and Exchange Commission classifies variable annuities as securities since the performance is originated from supplies, bonds, and various other investments.

An annuity contract has two phases: a buildup phase and a payout phase. You have numerous choices on exactly how you add to an annuity, depending on the annuity you purchase: enable you to select the time and quantity of the repayment.

{kind=link}

Latest Posts

What are the benefits of having an Deferred Annuities?

Where can I buy affordable Variable Annuities?

How can an Annuity Withdrawal Options protect my retirement?